Every six months, the biggest asset managers in the world publish their outlook. PGIM, which runs $1.3 trillion, just released theirs for mid-2026. It is a well-written document. The data is solid. The analysis is careful.

It is also, if you read it from a different angle, a useful map of who wins in the economy they are describing, and who does not.

Their headline thesis: we are in a "New Yield Paradigm." Rates are staying high. Inflation is sticky. The AI boom is driving investment at a pace not seen since the dot-com era. Their recommendation: own real assets, own equities, own credit. Be selective. Focus on alpha, not beta.

That is reasonable advice if you have assets to allocate. The question is what the same environment means for everyone who does not.

The inflation that will not go away

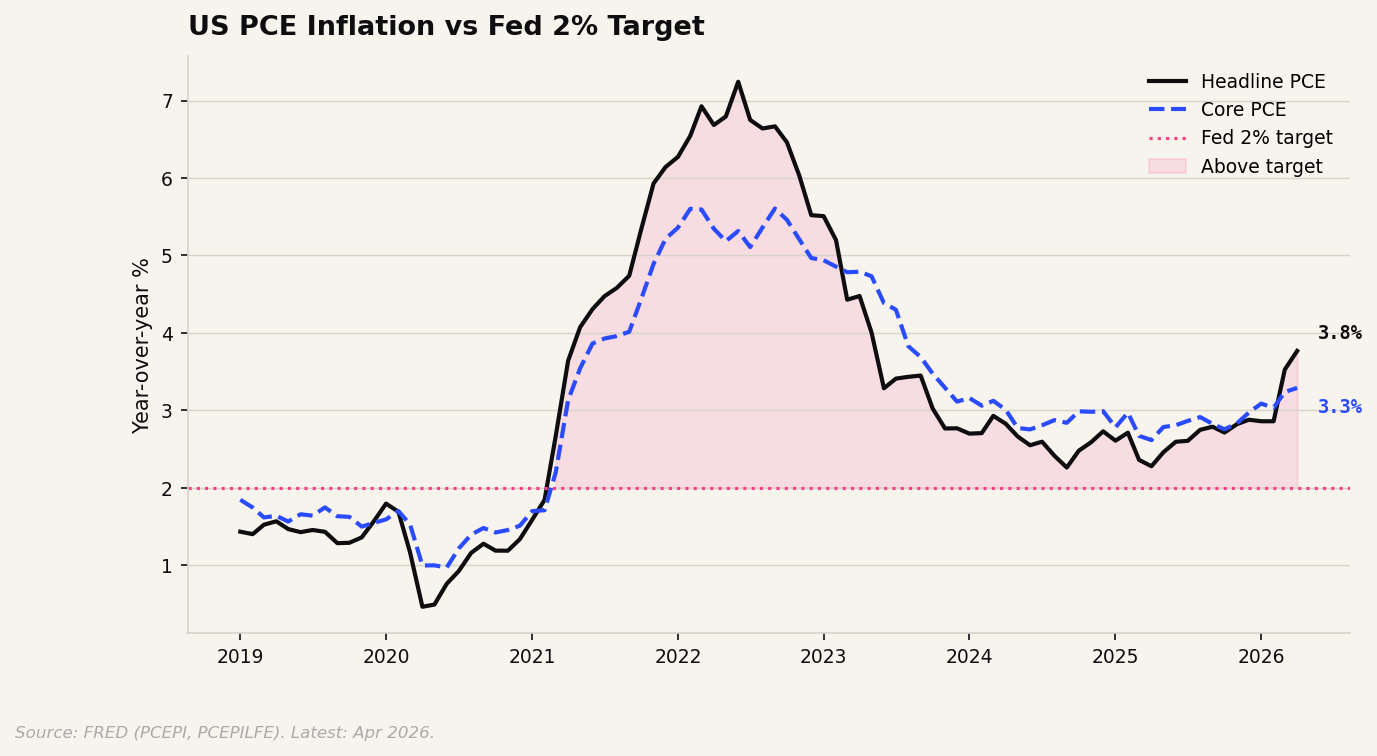

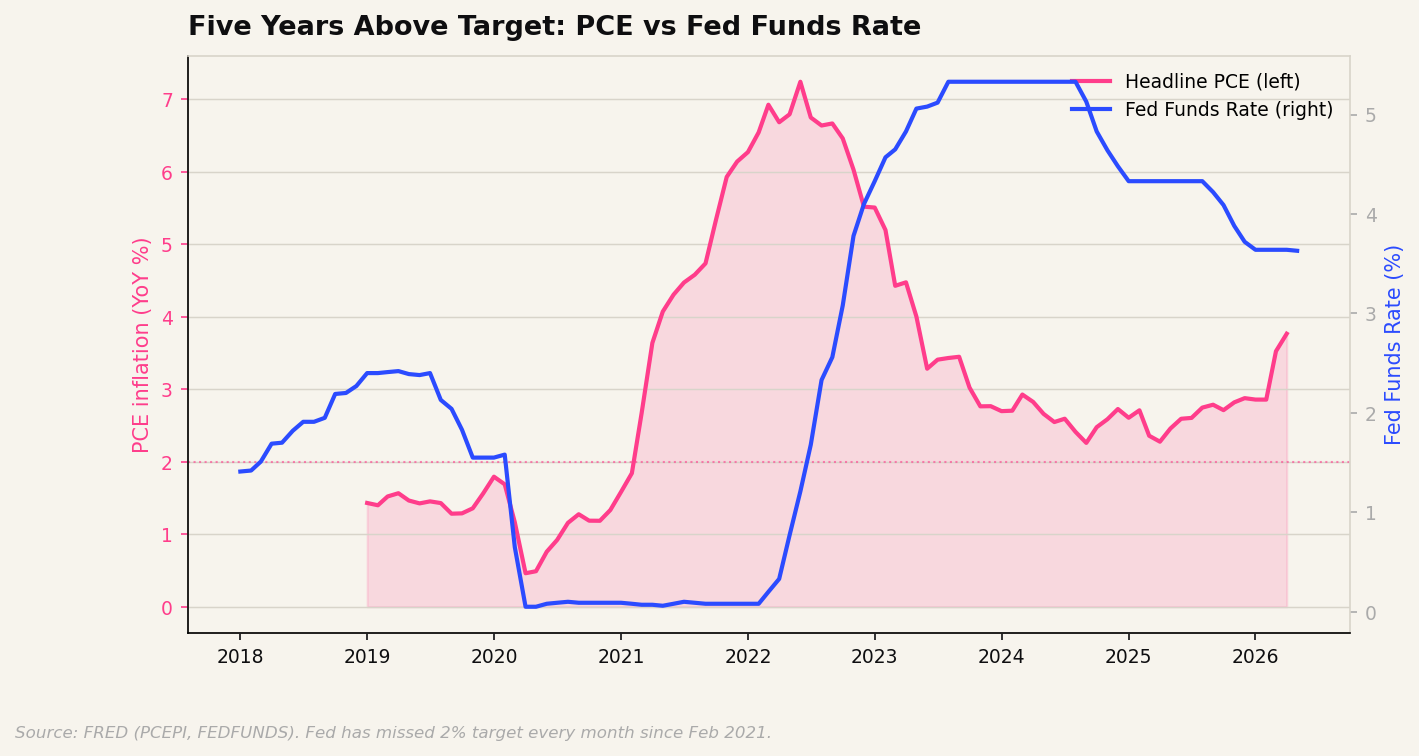

The Fed has a 2% inflation target. It has missed that target to the upside every single month since February 2021. That is five years and counting.

As of April 2026, headline PCE inflation sits at 3.8%. Core PCE, which strips out food and energy, is at 3.3%. Both are nearly double the target.

PGIM expects the Fed, under new Chair Kevin Warsh, to raise rates three more times this year. The reason the Fed is raising rates is to slow inflation. The reason inflation is sticky is partly the AI buildout, which is pumping enormous amounts of capital spending into an economy that is already running hot. The irony is that the same boom making investors bullish is also the thing keeping prices elevated for everyone else.

Here is the part that does not appear in most market outlooks: a 3.8% inflation rate is a tax. It falls hardest on people whose income is fixed, whose savings are in cash, and who cannot afford to move wealth into the financial assets that keep pace with or outrun it.

The Fed has a model for this. It is called the "wealth effect," and PGIM references it explicitly. When asset prices rise, wealthy households feel richer and spend more. That is a feature of the current economy, not a bug. The question is what the other side of that looks like.

Five years of running behind

Here is a cleaner way to think about it. If you had $100,000 invested in the S&P 500 at the start of 2021, that money has more than kept pace with inflation. If you had $100,000 in a savings account earning the average US savings rate over the same period, you have lost significant real purchasing power. Not because anything dramatic happened to you. Just because inflation compounded quietly while your cash sat still.

PGIM's document is written for the first group. That is not a criticism, it is a statement of purpose. But it is worth naming.

Who actually owns what

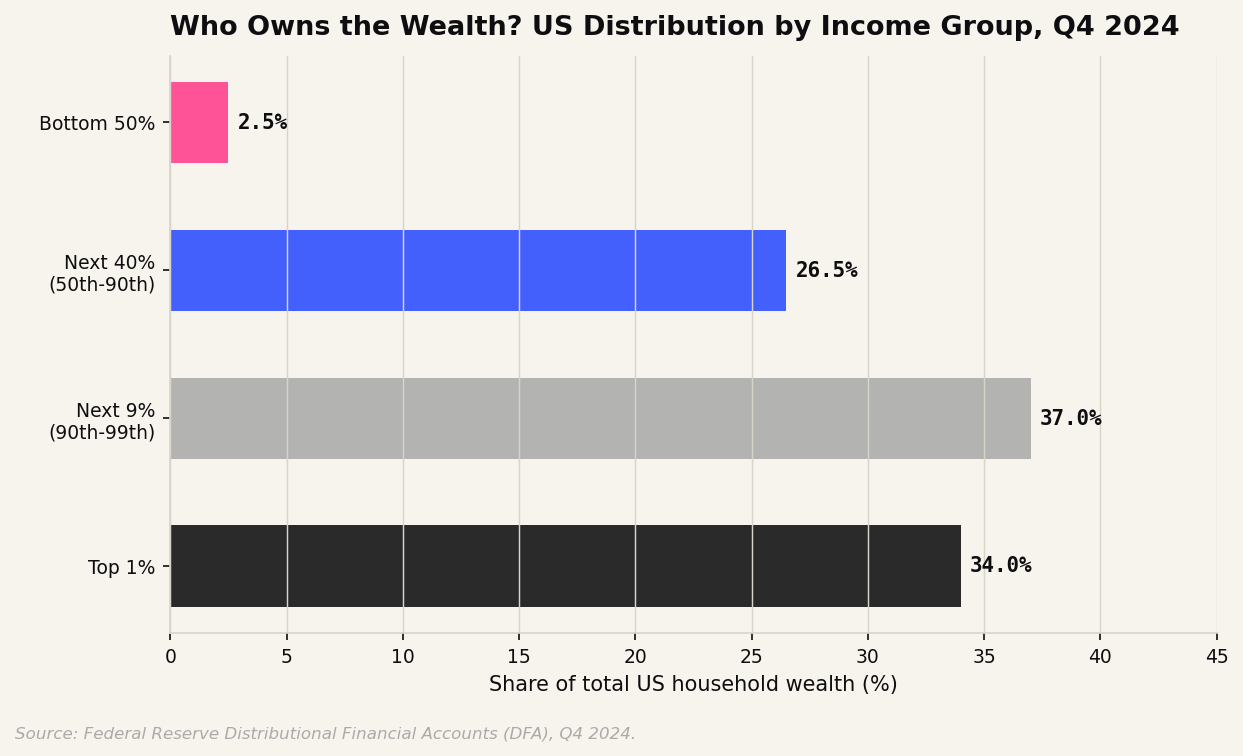

The "wealth effect" driving upper-income consumer spending that PGIM highlights has a precondition: you have to own wealth. Here is what that looks like in the US.

The top 1% owns 34% of all US household wealth. The next 9% owns another 37%. That means the top 10% controls 71% of the wealth that rises when asset prices go up.

The bottom 50% of households, collectively, own 2.5%.

When PGIM says "wealth effects continue to power spending among upper-income households," they are describing a real phenomenon. It is just a very concentrated one.

This is the measurement problem that does not show up in GDP. The economy can be growing, inflation can be elevated, asset prices can be rising, and all of those things can be simultaneously true while the median household is falling behind. Not because of a recession. Because of arithmetic.

The AI capex surge and what it actually is

PGIM's most striking data point: business investment in tech and information processing is approaching the levels seen at the peak of the 1990s telecom boom.

That is a big number. The 1990s buildout, at its peak, was one of the largest capital investment cycles in US history. The current AI buildout is approaching that scale.

What this means in simple terms: an enormous amount of capital is being spent on computing infrastructure. That spending is a tailwind for companies in the AI ecosystem, for shareholders of those companies, and for anyone whose income or savings are tied to that sector.

What it is not, yet, is a broad-based productivity boom that raises wages for the median worker. PGIM acknowledges this explicitly: "while AI may eventually lift productivity growth and push inflation lower, the demand-side boom in AI investments is colliding with ongoing supply-side constraints and boosting inflation well above the Fed's target."

Eventually is doing a lot of work in that sentence.

The K-shape, named and unnamed

Buried in PGIM's section on China is a phrase they use to describe the Chinese economy: "a K-shaped, two-speed economy." Rich urban areas recovering, lower-tier cities lagging. High-end consumption resilient, broad consumer sentiment weak.

They do not use that phrase to describe the United States. But the data they present for the US tells a similar story. AI-driven wealth effects powering upper-income discretionary spending. Payrolls growing, but real wages being eroded by persistent inflation. The Fed tightening to control price growth, which raises borrowing costs for everyone who does not already own assets.

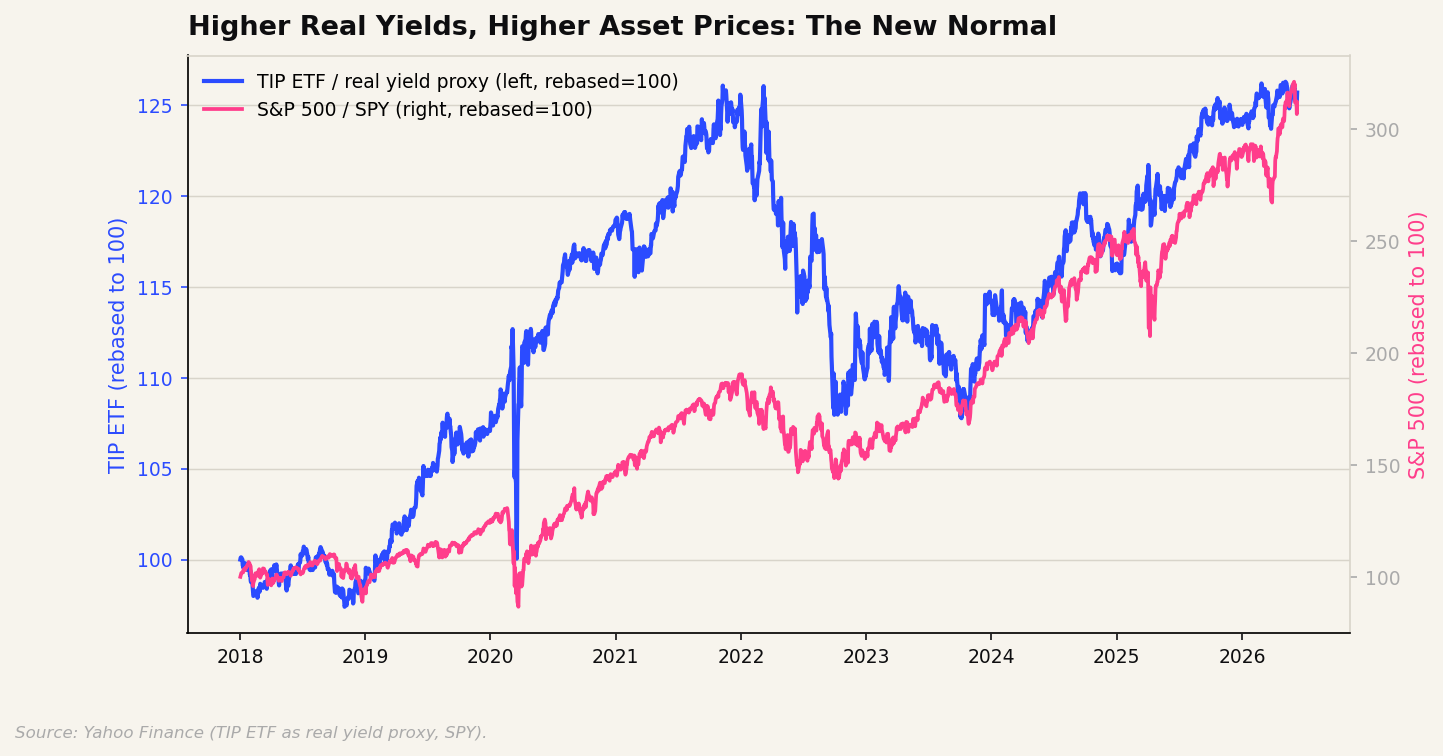

The unusual thing about the current cycle, visible in the chart above, is that real yields and equity prices have been rising together. In the decade after 2008, low rates drove asset prices up. Now higher rates are arriving at the same time as a massive investment boom, and assets are still rising, because the boom is generating returns that justify higher discount rates.

That is good news if you own equities. It is complicated news if you are trying to buy a house in an environment where mortgage rates are elevated and home prices have not come down.

What PGIM is actually saying

Let me be direct about what the recommendations in this report add up to.

"Real assets, such as real estate, commodities, and infrastructure, offer a partial hedge against elevated inflation." These are the assets most ordinary households cannot easily buy.

"Global growth equities to harness prevailing tailwinds." You need a brokerage account and some capital to harness tailwinds.

"High-quality securitized credit, including asset-based finance and CLOs." This is capital earning returns from other capital, and it is not available to retail investors in most forms.

None of this is cynical. PGIM is doing its job. The recommendations are sensible for institutional allocators in the environment that exists. The environment that exists is one where, as our previous piece documented, the labour share of US GDP is at a 70-year low, the return on capital persistently exceeds economic growth, and the asset price trap has been closing for three decades.

The institutional consensus has now priced all of that in. The recommendation is to own the trap.

The hot take, tested

There is a version of this that circulates on financial social media: the Fed doesn't care about regular people, only about markets.

That is too simple. But here is the version that holds up to the data.

The Fed's primary tool is interest rates. Raising rates slows inflation by slowing borrowing and spending. It also raises the cost of mortgages, car loans, and small business credit. It raises the return on financial assets relative to wages. The mechanism that cools inflation is the same mechanism that advantages capital over labour.

The Fed knows this. PGIM knows this. The financial system is not designed to be cruel. It is designed around the assumption that rising asset prices eventually produce broad prosperity through investment and employment. Sometimes that works. The data from the last five years suggests the lag is longer, and the distribution more unequal, than the models assumed.

PGIM's outlook is the institutional version of that knowledge, expressed as a buy list.

Data: FRED (PCEPI, PCEPILFE, FEDFUNDS, DFII10); Federal Reserve Distributional Financial Accounts Q4 2024; PGIM 2026 Mid-Year Global Market Outlook. This piece is independent analysis and is not affiliated with or endorsed by PGIM.