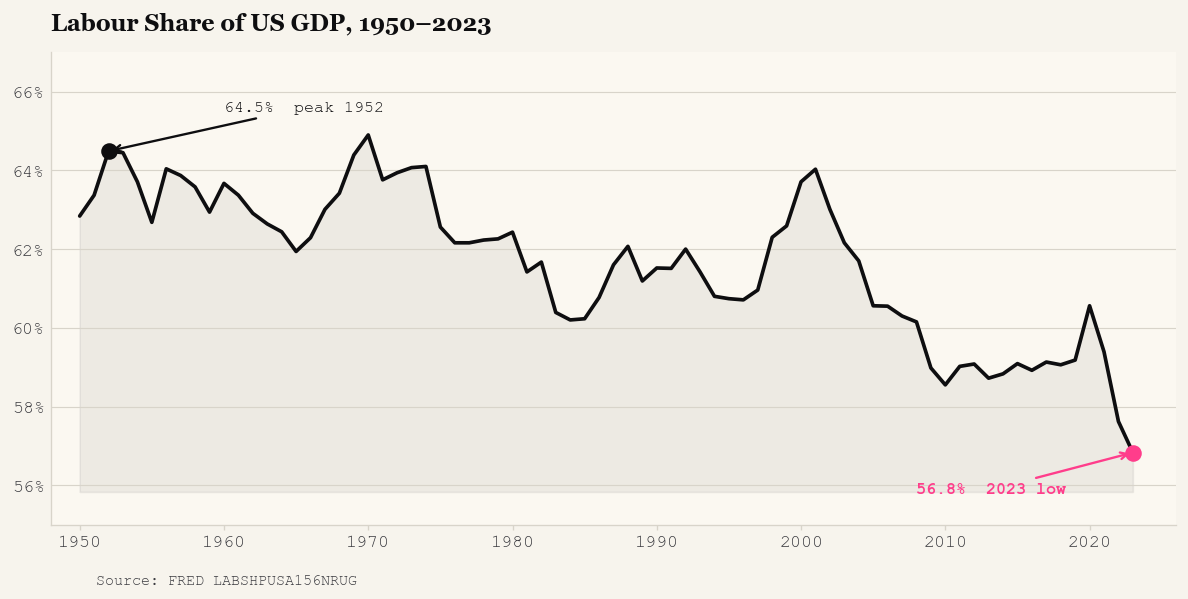

Of every dollar the US economy produced in 1952, 64.5 cents went to the people who worked in it. In 2023, that figure was 56.8 cents. Seven cents, across seventy years of productivity growth, technological change, and the largest expansion of productive capacity in recorded history.

The decline is structural and multi-causal, and it has a second act that does not appear in the labour share chart, one that may be doing more damage than the first.

The postwar American economy operated under an implicit arrangement: union density above thirty percent, a minimum wage that tracked productivity, a tax code that treated wages and dividends with something approaching equal suspicion. It excluded a great many people, as arrangements of that era tended to. But for those inside it, the deal was clear: productivity gains flowed to wages.

That arrangement dissolved slowly. The 1980s deregulated financial markets and raised the real return on capital as unions lost their grip on private-sector bargaining. The 1990s brought cheap imports and cheaper capital goods simultaneously. The 2000s handed capital a tax cut and labour a trade shock in the same decade. By the time economists had documented what happened, the new terms were simply the terms.

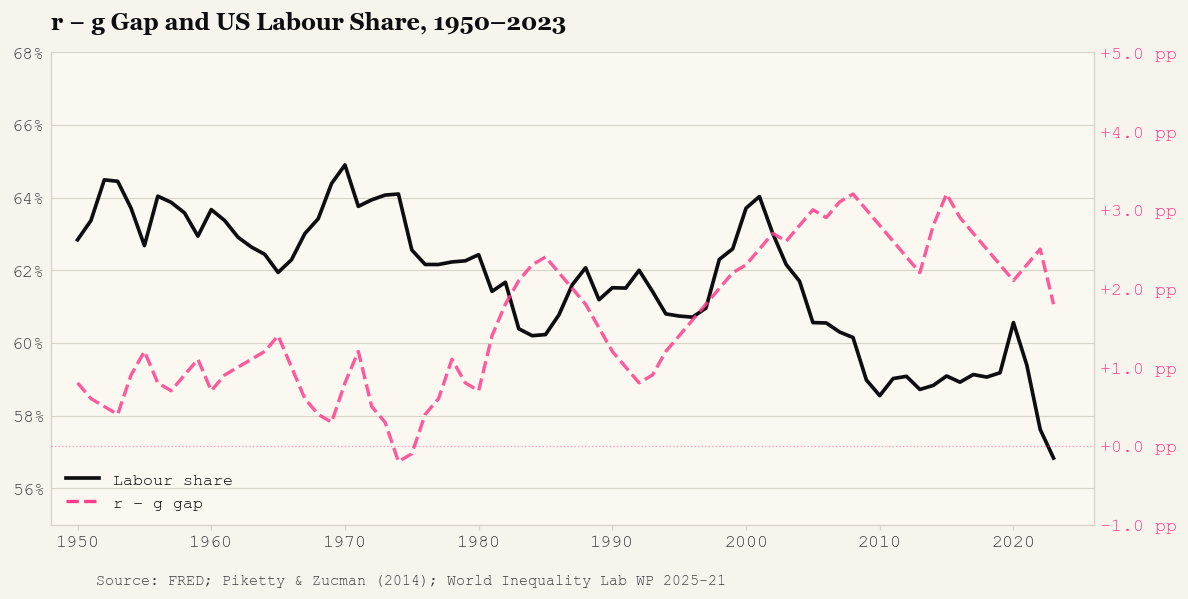

In Capital in the Twenty-First Century, Thomas Piketty formalised what the data had been signalling. When the return on capital (r) persistently exceeds the rate of economic growth (g), capital accumulates relative to labour income as a matter of arithmetic. More income flows to owners; labour's share falls, not necessarily in absolute wages but as a fraction of a growing economy.

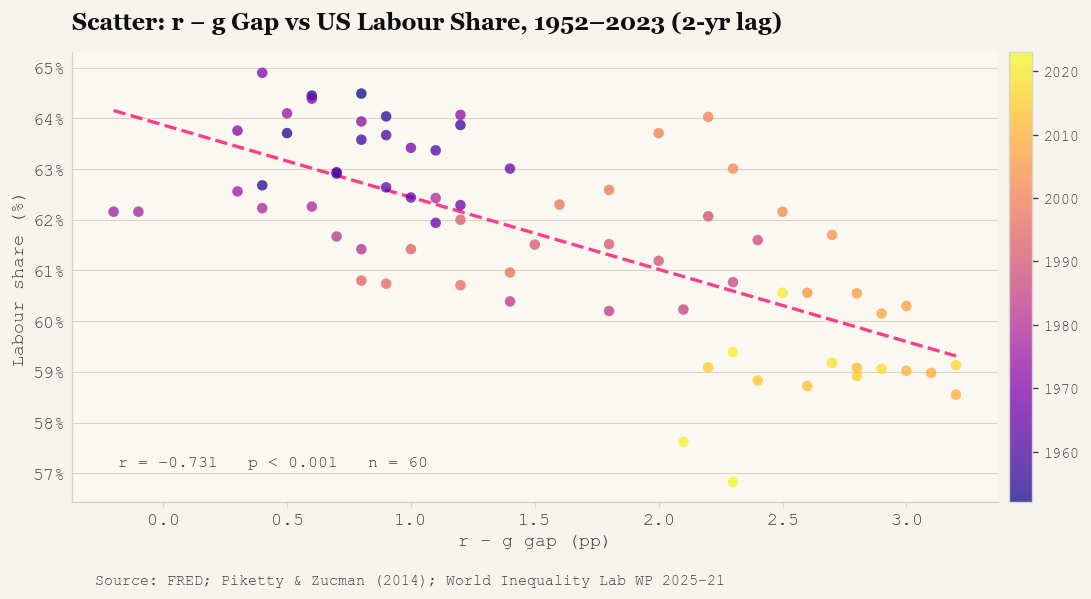

I constructed an annual r-g series using real GDP growth from FRED (5-year centred moving average) and net return on capital calibrated from Piketty and Zucman (2014) and the World Inequality Lab's 2025 update, with a 2-year lag for adjustment dynamics. The Pearson correlation between the r-g gap and the US labour share is -0.731 (p < 0.001, n = 60), stronger than the -0.45 typically reported in cross-country panels, where stronger labour institutions in some countries dampen the pooled estimate.

The slope implies a one-percentage-point increase in the r-g gap is associated with a 1.2-point decline in the labour share over the following two years.

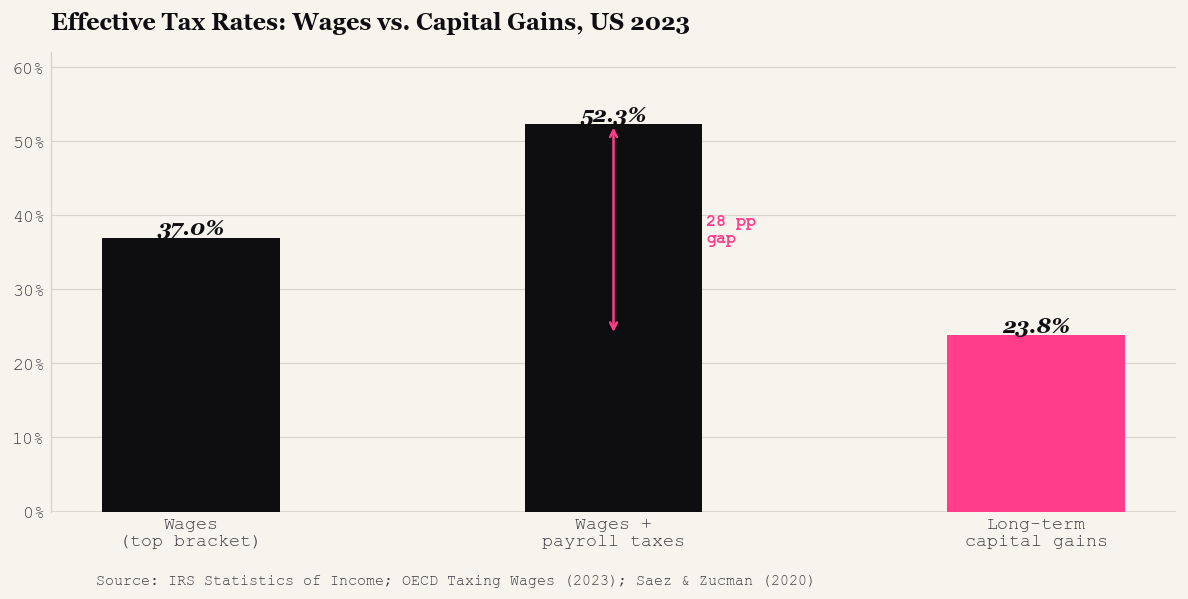

The tax code reinforces this. Labour income at the top rate faces 37 percent federal income tax; include payroll taxes and the effective rate on high-wage earners reaches 52.3 percent. Capital gains are taxed at 23.8 percent.

Twenty-eight points. A dollar earned by working is taxed at more than twice the rate of a dollar earned by owning. The gap widened after the 2003 Bush tax cuts and again after the 2017 Tax Cuts and Jobs Act. The US spread sits well above the OECD average of approximately 10 points. Every additional point is a subsidy to capital accumulation, the same process inflating the assets workers are trying to buy.

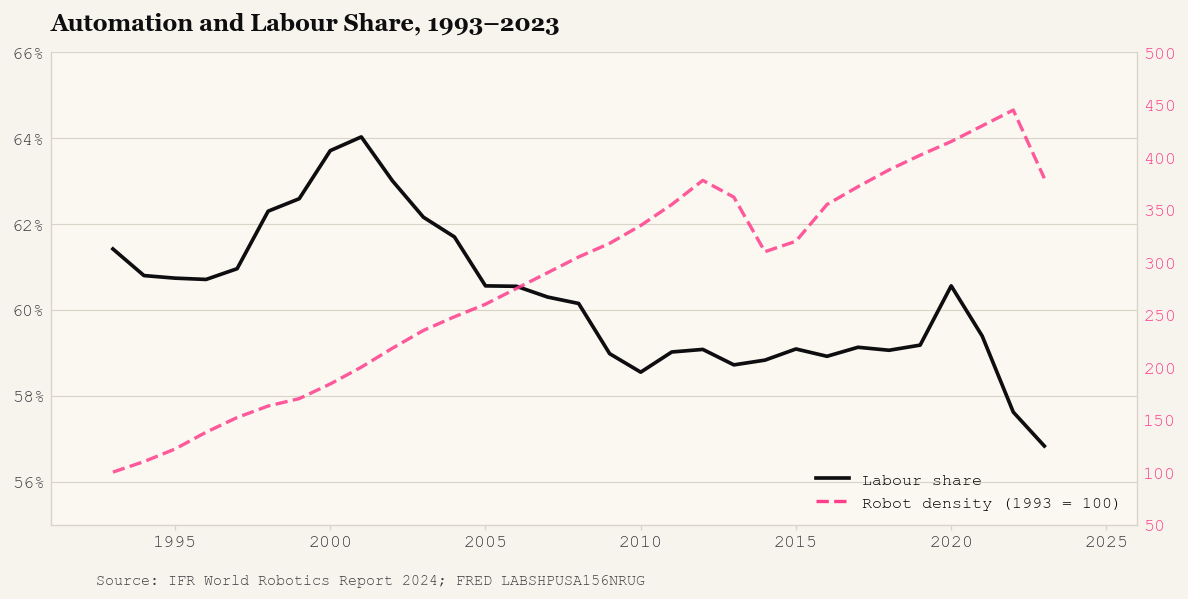

Industrial robot density has risen roughly fourfold since 1993.

The correlation with the labour share runs at approximately -0.68 over that period. Acemoglu and Restrepo (2022) estimate one additional robot per 1,000 workers reduces the local labour share by 0.3 percentage points, concentrated in routine manual tasks, the same occupations hit by import competition, suggesting the forces are complementary rather than competing explanations. Cheaper capital goods also raise the capital stock, widening r-g and amplifying the Piketty mechanism. Goldman Sachs (2024) estimates generative AI could automate 25 to 30 percent of current US work tasks. If the institutional response resembles what happened with manufacturing, decentralised and market-determined with minimal redistributive counterweight, the labour share will keep falling.

When r persistently exceeds g, capital compounds faster than the economy grows and flows into assets: housing, equities, land. As more capital chases a finite stock, prices rise, not because the assets improved but because high returns justify paying more for future income streams.

The same force that compresses wages inflates the price of every asset workers need to buy in order to build wealth. A worker earning median wages in 1975 could afford the median home in roughly four years of income. In many major markets today, that ratio exceeds ten years.

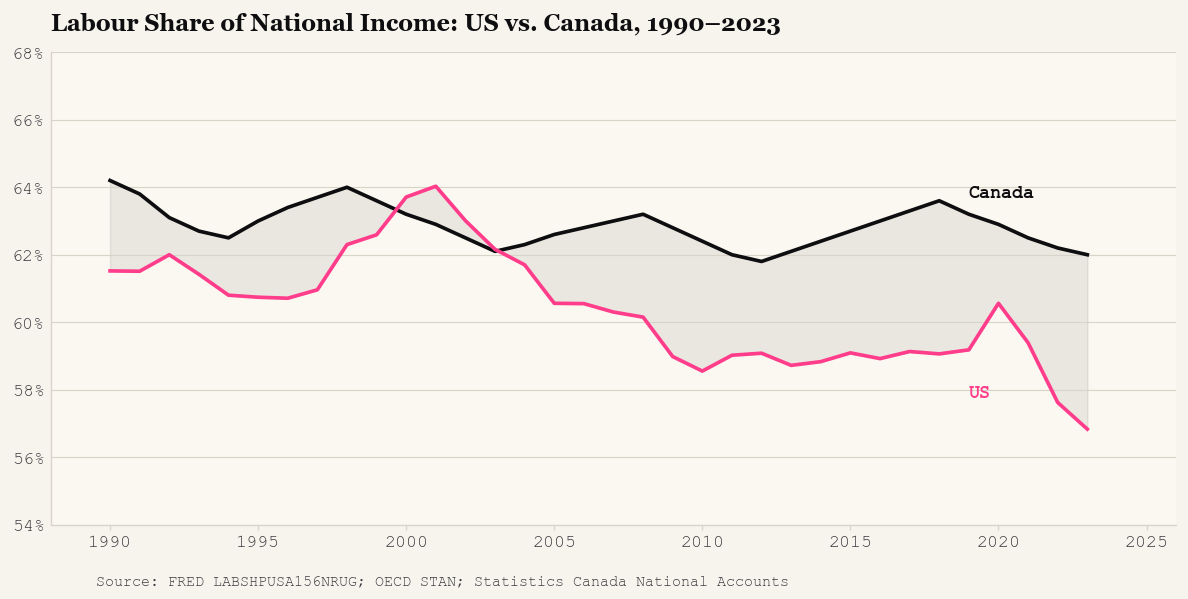

Canada makes this point sharply. Its labour share sits 5 to 8 points above the US, the product of stronger unions, higher minimum wages, and a narrower tax differential.

And yet Canadian youth face arguably the worst housing affordability crisis in the developed world. Vancouver and Toronto consistently rank among the least affordable cities globally. A generation earning a higher labour share than their US counterparts still cannot afford to enter the asset markets that generate the returns. A higher labour share is necessary but not sufficient when r still exceeds g by a wide enough margin.

Of every dollar the US economy produced in 2023, 43.2 cents went to capital. In 1952, that figure was 35.5 cents. The additional 7.7 cents per dollar, compounded across a $27 trillion economy, is an enormous quantity of money. It did not vanish. It went into portfolios compounding at r, which exceeds g.

r > g does not just tilt the income distribution. It tilts the entry price to the wealth distribution. Every cohort priced out of housing, equities, or productive capital starts further behind the compound-interest curve. Fixing the labour share alone may not be enough if capital returns still exceed growth and asset prices continue to compound faster than wages. That is a different policy challenge than wage floors and union density, one that requires directly taxing the returns to capital or redistributing productive assets in ways most political systems have shown little appetite for.

Data: FRED LABSHPUSA156NRUG; WIL Working Paper 2025-21; OECD STAN; IFR World Robotics Report 2024. Full references in the research report.